S&P500 Trading Update 13/5/26

S&P500 Trading Update 13/5/26

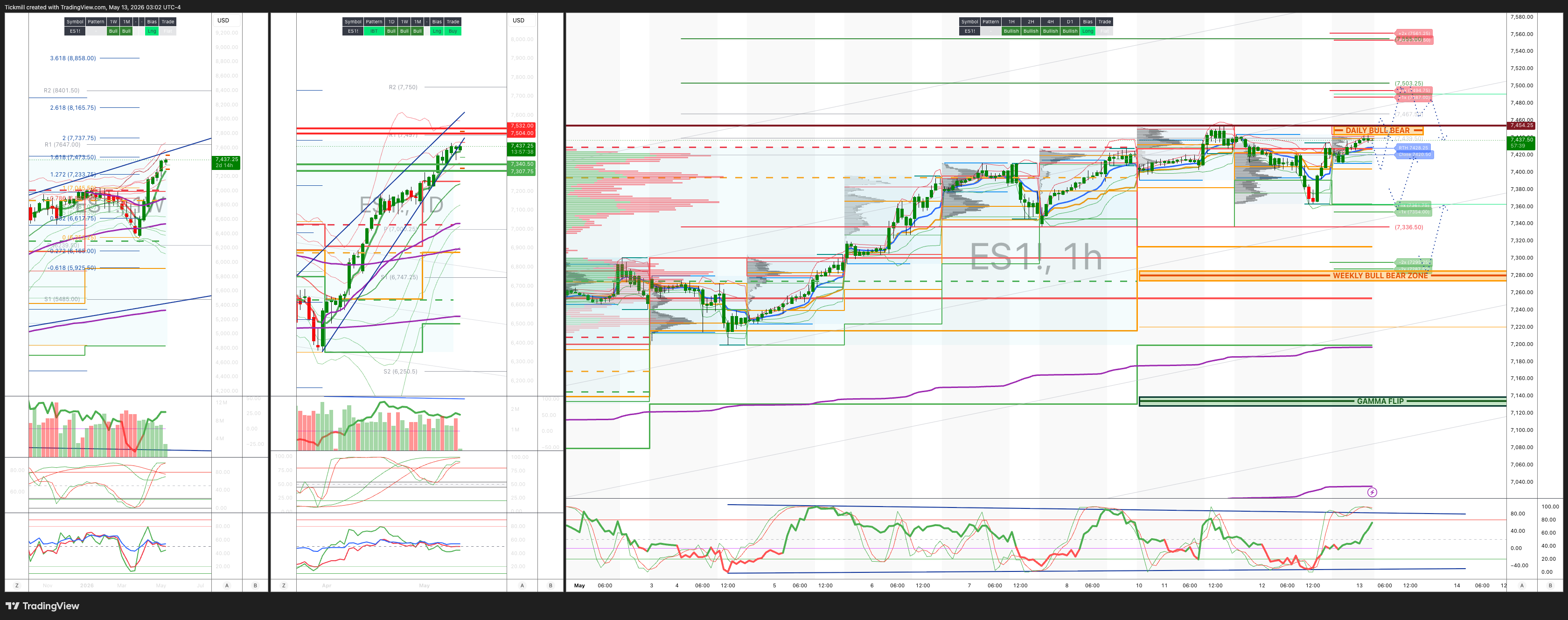

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7280/70

WEEKLY RANGE RES 7504 SUP 7340

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.2 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7410

WEEKLY VWAP BULLISH 7255

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – BALANCE 7454/7327

WEEKLY STRUCTURE – OTFH - 7199

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7455/45

GAMMA FLIP 7135

DELTA FLIP 6932

DAILY RANGE RES 7494 SUP 7361

2 SIGMA RES 7553 SUP 7287

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

LONG ON ACCEPTANCE DAILY BULL BEAR ZONE TARGET DAILY/WEEKLY RANGE RES

SHORT ON REJECT/RECLAIM DAILY/WEEKLY RANGE RES TARGET 7455

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

JPM TRADING DESK VIEW - ‘Tactically Bullish’

US / EU Market Intel: Semi Digestion, Oil-Driven Rates Pressure, Defensives Lead

US equities closed lower but finished well off the intraday lows after a strong afternoon rebound. The S&P 500 ended -16bps, but the weakness was concentrated: Semis -3.8%, Cyclicals -2.2%, and Tariff Short -2.2% lagged, while Defensives +1.4% outperformed. Importantly, 51% of S&P stocks finished higher, and 6 of 11 sectors closed green, so the headline index loss overstated the breadth of the damage.

The main drivers were semi/AI weakness, the Korea selloff, higher oil, hotter US CPI, and higher yields. But the afternoon rebound suggests this was more of a positioning-driven digestion than a fundamental break.

Key market moves

S&P 500: -16bps, off intraday lows

Semis / SOX: -3.8%, after being down as much as -6.8%

Cyclicals: -2.2%

Defensives: +1.4%

WTI crude: +USD 4.10 to USD 102.13

US 2Y yield: +3.6bps

US 10Y yield: +4.9bps

Europe: weaker across the board: SX5E -1.5%, SXXP -1.0%, DAX -1.6%, UKX flat

European weakness was broader, with underperformance in Semis, Electrification, Stagflation Short, and Momentum Long. Higher oil, hotter US CPI, and UK political uncertainty around Starmer pushed yields higher, with 2Y gilt yields +8bps and 2Y bund yields +7bps.

Main message

Today’s weakness does not look like a fundamental regime shift. It looks more like a needed digestion after a sharp AI/semi rally, amplified by crowded positioning and macro noise. The key risk is that higher oil and higher yields start to pressure multiples and the consumer. But the afternoon rebound, positive S&P breadth, and dip-buying in tech suggest investors are not abandoning the AI trade. They are becoming more selective.

Semis: first real wobble in weeks

Semis had their first meaningful pullback after weeks of strong performance. The SOX fell 3.8%, though it recovered from an intraday low of -6.8%. Investors blamed Korea AI tax headlines, Iran/oil risk, higher yields after CPI, crowded AI/memory positioning, and recent double-digit rallies across AI themes.

The cleaner interpretation is that the sector was due for a pause. The desk noted limited flow panic and buyers stepping back in during the weakness. Beta was hit, but momentum held up relatively well. Some underperforming optical names bounced. Software outperformed, though with some SMID weakness in names like GTM and GTLB. Long-only demand is starting to appear in enterprise SaaS, and software was the desk’s largest buy sector on the day.

Korea selloff: headline shock, then clarification

The Korea selloff contributed to pressure on global AI and semis. EWY fell 7.4% after a top South Korean policymaker suggested the country should pay citizens a dividend using taxes on AI profits. That raised fears of a windfall tax on AI-related corporate profits.

But the comments were later clarified: the proposal was about using excess tax revenue generated by the AI boom, not necessarily creating a new direct levy on companies. An official also said the remarks were personal opinion and not part of formal policy discussions. So the Korea move was damaging for sentiment, but the underlying policy risk may have been overstated.

Iran: deal still looks far away

Iran headlines remain a key macro overhang. Semi-official Fars News reported that Iran will not join US talks without five preconditions: ending the war on all fronts, especially Lebanon; lifting anti-Iran sanctions; releasing Iran’s frozen funds; compensating Iran for war damages; and accepting Iran’s sovereignty over the Strait of Hormuz.

The last two are especially difficult for the US to accept, implying a near-term deal remains unlikely. The Trump-Xi summit is still a wildcard, but Trump has downplayed Iran as a main topic and suggested trade will be the top priority. Reports that Kharg Island oil shipments remain idle could also increase pressure on Iranian storage and keep oil risk elevated.

CPI: fine for now, but not harmless

The CPI print was not disastrous, but it was not clean. The market can still look through much of the increase because it was heavily driven by energy, which is viewed as potentially transitory if the Iran/oil shock fades. Energy drove roughly 40% of the increase, while food was also notable. Shelter surprised to the upside, core goods were soft, and core services ex rent/OER remained firm.

JPM Economics estimates core PCE +0.23% m/m, with year-over-year core PCE around 3.2%, close to 3.3%. The main risk is that if next month’s inflation print accelerates, the bond market may stop looking through it. For now, CPI is manageable, but the combination of higher oil + sticky services + higher yields is a warning.

Rates: oil and CPI keep pressure on yields

US yields moved higher, with the 2Y +3.6bps and 10Y +4.9bps, driven by CPI and crude. The UK also matters: 2Y gilts are up 15bps over two days, driven by oil and political uncertainty around Starmer. If gilt volatility continues, it can spill into global duration markets, especially when the US bond market is already sensitive to inflation and fiscal concerns.

The equity market can tolerate moderate rate increases if earnings are strong. But it becomes harder for long-duration AI and semi multiples if oil keeps pushing yields higher.

CSCO earnings: memory costs and AI demand in focus

Cisco reports after the close tomorrow. The setup is not expected to be especially dramatic, but it matters for the broader AI infrastructure narrative. Investors will focus on memory cost pressure, FY26 revenue guidance, AI networking demand, margin resilience, Splunk’s subscription transition, the security business, and Cisco’s ability to manage costs and pricing.

Positioning is modestly short, with a positioning score of -2 and implied move of +5.7%. Buy-side expectations are not high. Investors expect perhaps a slight AI revenue beat, but remain cautious on networking revenue and margins due to memory cost pressure and unfavorable mix. For the broader market, the most important read-through is whether higher memory costs are becoming a margin issue across AI infrastructure.

Consumer: low-end may be forming a tactical bottom

Consumer discretionary remains under pressure. ONON and UAA are the latest names to miss expectations, adding to concerns after recent weakness in lower-end consumer names. The pressure points are hotter CPI, rising oil and gasoline prices, weak low-end consumer data, rotation away from consumer into AI, and margin uncertainty.

However, some low-end plays may be nearing oversold levels. JPM’s low-end consumer index has a 14-day RSI around 30, long/short ratio at the 25th percentile, and net exposure at -0.08z. There is some early demand emerging in select retail names, though conviction remains low. Staples are seeing demand in higher-quality names like KO, PM, MDLZ, PG, KDP, and MNST.

Financials: long-only investors still constructive

Long-only investors remain fairly constructive on financials. They are not flagging major credit issues, recent quarters have been clean from an asset-quality standpoint, and investors remain comfortable with the macro backdrop. AI-related risks are increasingly discussed, but more as operational or competitive risks than near-term earnings risks. Financials still look relatively insulated from the Middle East conflict and may benefit from capital markets volatility if credit stays benign.

Energy and momentum: clean energy squeeze

Momentum has been extremely strong. JPM’s long/short momentum pair rose 6.3% in one day, one of the largest moves on record and the biggest since August 2022. In energy, this is showing up largely in clean energy. JPM’s clean energy index rose roughly 10% over two days, the largest two-day move in seven months.

This fits the broader market structure: high oil, AI power demand, electrification, and factor momentum are combining to create sharp moves in energy-adjacent and power-related themes.

JPM Market Intel view: tactically bullish, but take some tech profits

JPM Market Intel remains tactically bullish, based on a resilient macro backdrop, strong earnings, renewed tech interest, potential Xi-Trump agreements, and the possibility of a deal reopening the Strait of Hormuz. But after the sharp tech move, the desk suggests taking some profits and using call overwrites to maintain upside while reducing downside risk.

The preferred framework remains a barbell: long secular tech / AI winners, selective cyclicals especially financials, precious metals and miners, plus hedges via oil, energy, VIX calls/call spreads, and index puts/put spreads.

The biggest risks to the bullish view are renewed Middle East escalation, a spike in bond yields or bond volatility, a material reversal in tech, a momentum/beta unwind, and systematic funds reducing longs.

Trading takeaways

Stay constructive on AI infrastructure, but reduce chase risk. Use call overwrites or spreads in crowded tech winners. Watch CSCO for AI networking, memory-cost, and margin read-throughs. Keep oil/energy upside as a hedge against Middle East escalation. Maintain precious metals exposure, especially gold and miners. Be selective in consumer; low-end may be oversold, but conviction remains low. Financials remain a reasonable buy-the-dip area if credit stays benign. Keep index downside or VIX protection while oil and rates are rising.

Bottom line

Today was a semi-led positioning shakeout, not broad fundamental deterioration. The S&P closed only modestly lower, breadth was better than the headline suggested, and dip-buying returned in the afternoon. That said, the macro setup is getting more complicated. Oil above USD 100, sticky CPI components, higher yields, and unresolved Iran headlines create a less forgiving environment for crowded AI trades. The bull case remains intact, but it now requires more discipline: monetize some tech strength, keep hedges on, and focus on quality AI infrastructure rather than chasing every high-beta move.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!