The FTSE Finish Line 17/10/25

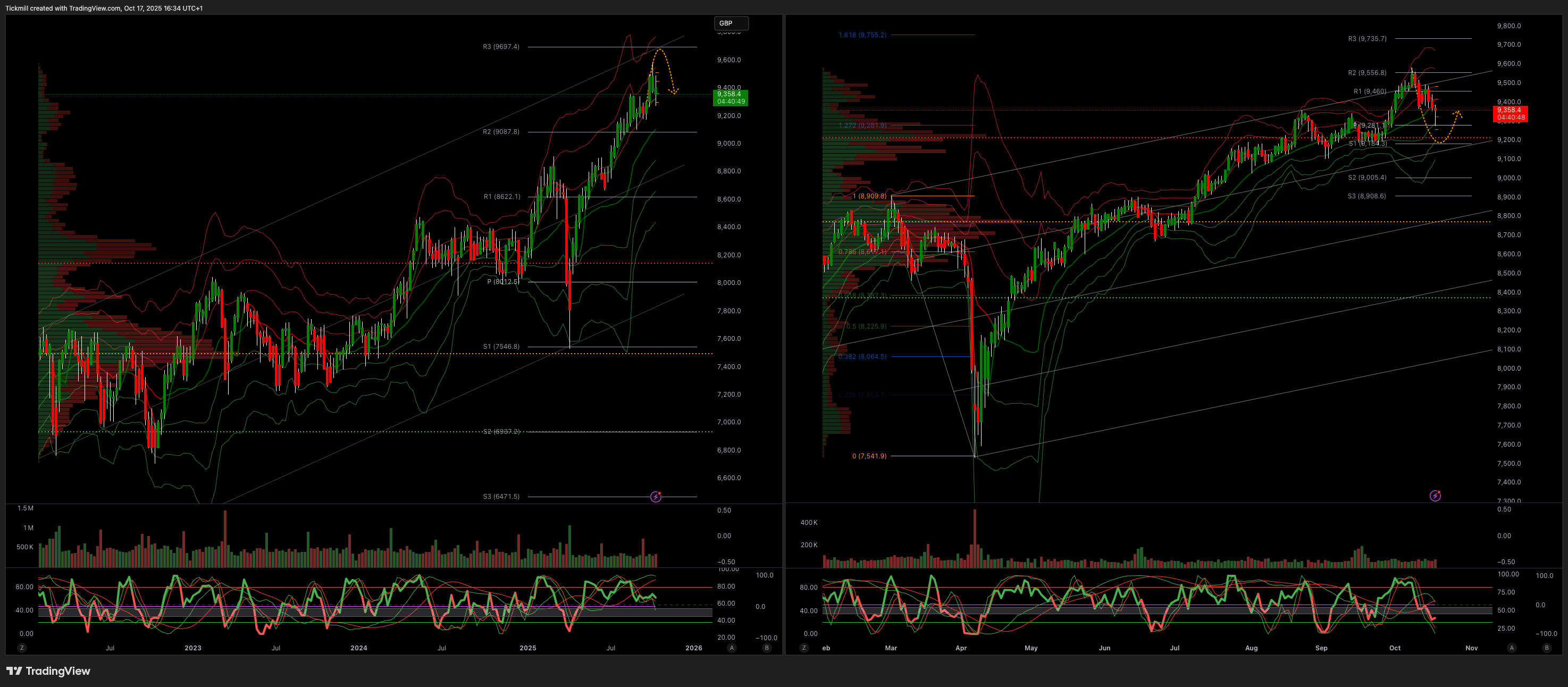

London's leading index slumped to a two-week low on Friday, dragged down by significant losses in oil giants and major banks, as a global selloff in financial stocks intensified over concerns about the stability of U.S. regional banks. The banking sector took a heavy hit, tumbling nearly 3%. Among the hardest hit were HSBC, Barclays, and Standard Chartered, which saw their shares drop by 1.9%, 5.3%, and 4.6%, respectively. Investment banks and brokerages also struggled, with their index slipping 2%. Brokerage firm ICG suffered the steepest decline in the FTSE 100, plunging 6.4%.

Across the Atlantic, U.S. regional bank Zions Bancorporation disclosed a $50 million loss tied to two loans from its California branch, while Western Alliance revealed it had filed a lawsuit against Cantor Group V, LLC, alleging fraud. These developments heightened fears about credit quality, further unsettling investors. Wall Street futures pointed to another weak start on Friday, following Thursday’s losses.

In London, oil heavyweights BP and Shell also weighed heavily on the FTSE 100, with their shares dropping 2.7% and 0.9%, respectively, as global risk aversion sent oil prices lower. Meanwhile, despite August showing signs of economic growth in Britain, the market gloom overshadowed any optimism. Earlier this week, the International Monetary Fund projected that the UK’s economy would achieve the second-fastest growth among the G7 nations in 2025, trailing only the U.S. Adding to the negative sentiment, the aerospace and defense sector fell 3.1%, mirroring losses in European counterparts. The day’s widespread declines underscored the fragile mood across global markets.

The UK weighted average gilt yield has fallen by approximately 20 basis points within just a week. This significant development is likely being closely monitored by the Treasury. Based on the timing of previous fiscal events, it is estimated that the ten-working-day observation window used by the OBR to assess gilt yields and other market variables for the fiscal forecast likely closed earlier this week. As a result, part of the decline in yields would have been captured, though not entirely, if our assumption about the observation window is accurate.This is important due to the impact it has on projections for debt interest payments over the OBR’s forecast horizon. To put it into perspective, the difference in shifting the observation window by just a few days could amount to as much as £3 billion, depending on whether the sharp drop in gilt yields is included. At this stage, it remains unclear exactly what dates the OBR selected, and therefore, how much influence this will have on the fiscal forecast. However, if the OBR is operating on a slightly later timetable than usual, capturing the lower gilt yields could reduce the Chancellor’s challenge of creating fiscal headroom by up to £3 billion. This, in turn, could slightly ease the burden of implementing tax increases.

The spotlight will be on the UK’s economic updates next week, starting with September’s public finance figures on Tuesday. While adjustments for VAT errors may address some recent inconsistencies, the broader picture is expected to show a continued overshoot compared to the Office for Budget Responsibility’s (OBR) projections. With the economy growing at a sluggish pace, government revenues might turn out to be more fragile than anticipated. Midweek, all eyes will be on Wednesday’s inflation report, which is likely to indicate a slight rise as persistent challenges in the services sector keep price pressures elevated. Adding to the mix, the long-awaited update on Producer Price Index (PPI) data, including the quarterly services measure paused since January, is also expected. The week concludes on Friday with retail sales figures, where the overall trend remains subdued despite some month-to-month variations.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!