Dollar Dumped On NFP Miss

Weak Jobs Data

The US Dollar is trading lower today on the back of the June NFP release yesterday which came in sharply below forecasts. The headline NFP reading fell to just 57k last month, well below the expected 114k reading the market was looking for. We also saw a sharp downward revision to the prior month’s 214k reading which was marked down to 129k, reflecting a much weaker jobs picture than initially thought, with additional downward revisions to the April data also. Ahead of the release, market pricing for a hike by year end (as per CME group Fed Watch) was around 85%. On the back of yesterday’s data, that pricing has now fallen to around 75% reflecting a cooling of tightening expectations.

Shifting US Inflation Outlook?

The shift lower comes at an interesting time for the Dollar. There has been a growing discourse over the last week or so regarding the build-up in tightening expectations and whether traders had become prematurely hawkish, particularly given the sharp drop in oil prices we’ve seen over the last month. Much of the narrative around hawkish Fed expectations is premised of upside inflationary risks given the ongoing US/Iran conflict and its impact on energy prices. However, with the two sides working on delivering a peace deal, oil prices have fallen around 30% in recent weeks and look set to fall lower if a deal is agreed. As such, there is a growing view that the Fed might not need to hike rates later in the year and yesterday’s soft jobs data seems to endorse that view, raising downside risks for USD near-term as tightening expectations are tempered further.

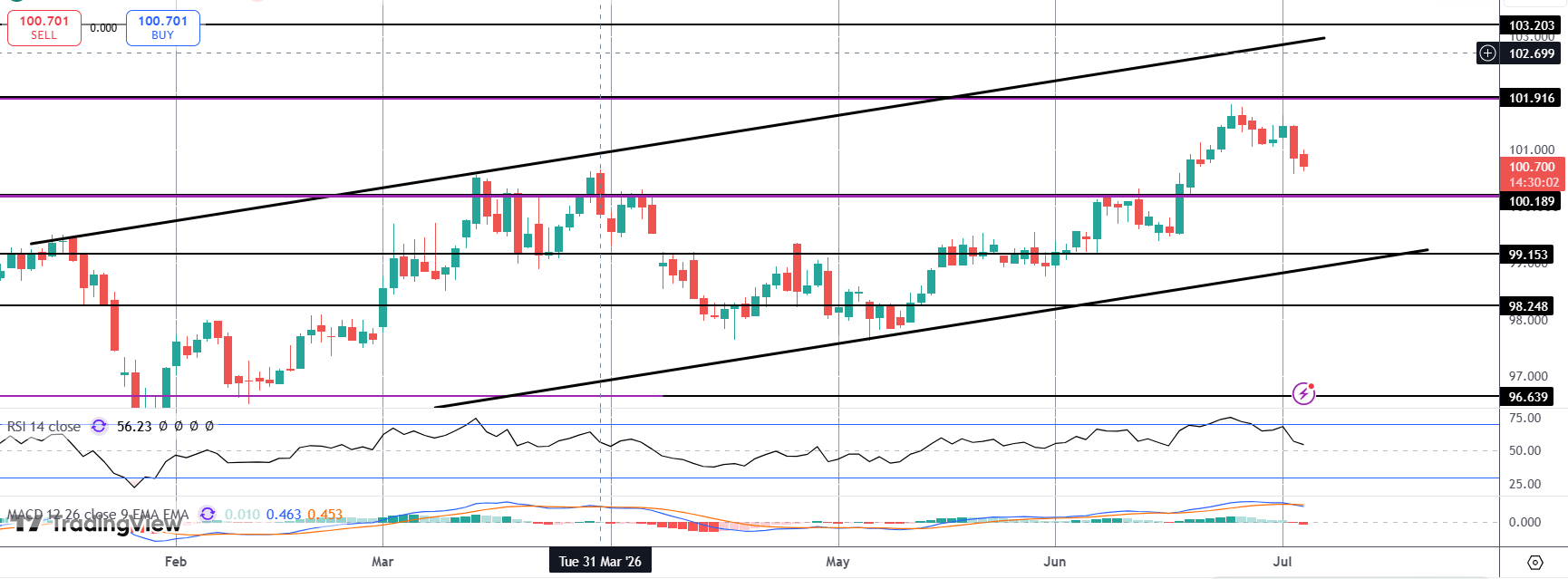

Technical Views

DXY

The rally in DXY has stalled for now into the 101.91 level with price since correcting lower. While we hold above the 100-mark, focus is on a fresh break higher towards the 103.20 level. However, if we break sub-100, focus turns to 99.15 as next support along with the bull channel lows.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.